Payday loans may seem ideal when you need some fast cash. But the high costs can leave you stuck in a debt cycle that’s almost impossible to escape.

Almost 80% of payday loan borrowers have to roll their original loan over into a new payday loan.

Table of Contents

What are Payday Loans?

Payday loans are small-dollar short-term loans that you can get from storefront lenders or online. They are usually repaid on your next payday. Payday loans sound relatively inexpensive because instead of stating the interest rate you’ll pay, you’re charged a “fee,” usually about $15 for every $100 borrowed. However, that works out to an APR of 365%. That’s extremely high compared to other types of loans, many of which have annual percentage rates capped at 36%.

Popular payday lenders include Speedy Cash, Advance America and Check ‘n Go.

READ MORE: Payday loan interest rates

Pro tip: Title loans are similar to payday loans, but they can be even more dangerous because the loan is secured by your vehicle. If you can’t make your payments as scheduled, your car will be repossessed.

How Payday Loans Work

Payday loans are easy to get. There are no minimum credit score requirements or credit checks. When you complete the application, you likely will have to grant access to your payday lender to debit the loan payment from your bank account on the due date. Some lenders may request a postdated check instead to ensure that they have a way to collect your debt.

READ MORE: How payday loans work

Tribal Payday Loans

Tribal payday loans seem similar to traditional ones, but they are much more dangerous. They’re based on Native American tribal land, meaning they have sovereign immunity. Tribal payday loans follow the laws established by the tribe rather than state laws.

This means that regardless of your state’s laws or interest rate caps, tribal lenders can (and will) charge you annual percentage rates as high as 800% – or even more.

READ MORE: Tribal payday loans

Why Do Payday Loan APRs Get So High?

Payday loan APRs are tricky, and how the APR is calculated depends on whether you have a traditional payday loan or a tribal payday loan.

Traditional Payday Loan APRs

Because payday loans are repaid in two weeks, there isn’t much time for interest to accrue, so lenders charge fees instead. The average fee ranges from $10 to $30 for each $100 borrowed, depending on the state in which you live and any state laws capping interest rates. These fees are high considering the money is only borrowed for two weeks.

- Paying $10 to borrow $100 equals an APR of 260%.

- Paying $30 to borrow $100 equals an APR of 782%.

But they’re not even close to the insanely high rates charged by tribal lenders.

READ MORE: Are payday loan interest rates fixed or variable?

Tribal Payday Loan APRs

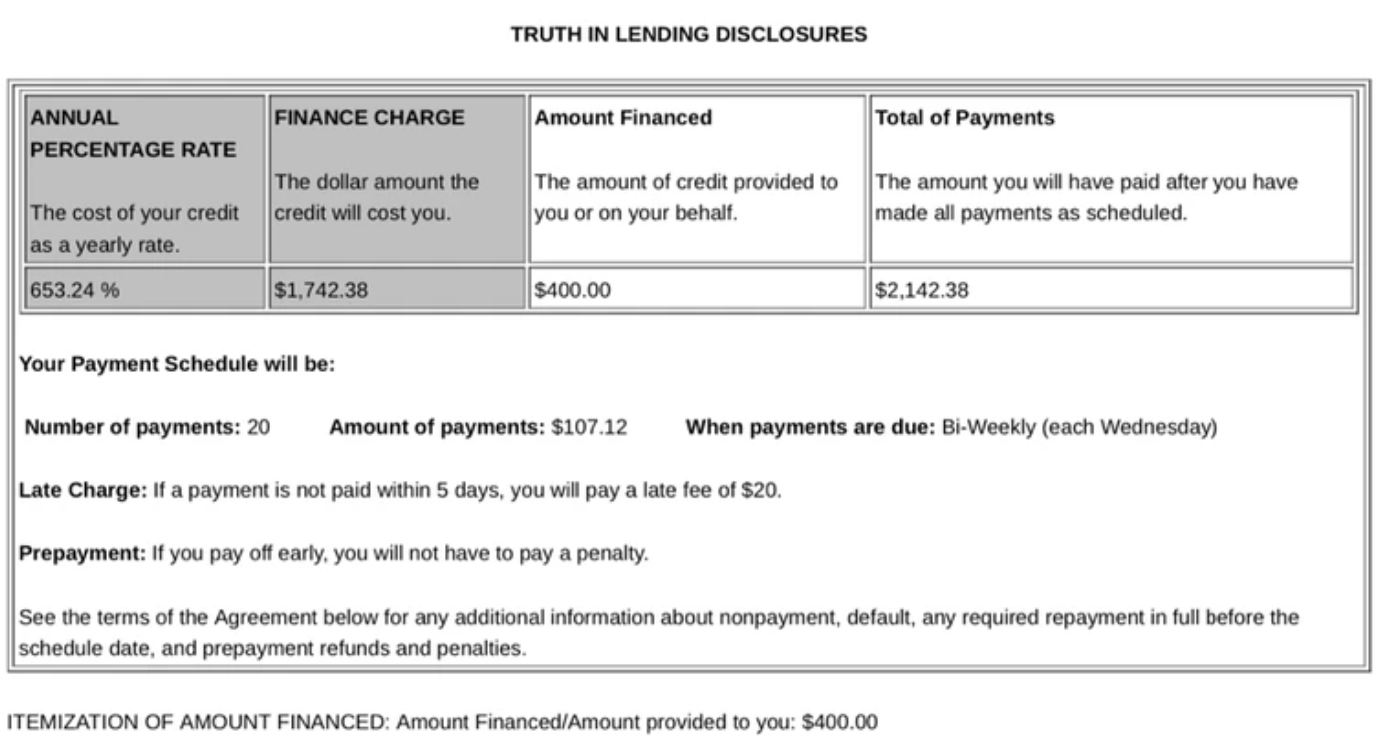

These are more complicated because they aren’t repaid in a lump sum. They’re short-term installment loans. The lenders use calculations over a calendar year to make it look like you’re paying the legal interest rate of 36%. It’s not until you get your loan agreement that they are legally required by the Truth in Lending Act to show you the full cost of borrowing. By that point, it is usually already too late to undo the damage unless you can repay your loan in full immediately.

When you borrow from a tribal lender, you’ll see something like this on your loan agreement:

You will pay more than $1,700 in interest over ten months of biweekly payments just to borrow $400. A traditional payday lender would charge a maximum of $120 in fees for the same loan.

Payday Loan Requirements

Most payday lenders ask for the following basic requirements:

- An active checking account

- Proof of income (pay stubs, etc.)

- Valid ID

- Be age 18 or older

- Some lenders will also require a Social Security number

READ MORE: Payday loan requirements

Why Was My Payday Loan Application Denied?

If you meet all of the payday loan requirements and have a steady source of income, it’s still possible for your payday loan application to be denied. Here are a few reasons that could happen:

- You can’t prove your income

- You don’t earn enough money

- You don’t have a checking account

- You didn’t pass a Veritec check

- You get paid in cash

- You’ve filed for bankruptcy

- You have other payday loans or paycheck advances

- You have blemishes on your accounts

- Your credit history is poor

- You don’t meet the lender’s additional criteria

- You’re in the military

- You have a joint account with someone who has bad credit

- You make payments to gambling sites

- You could be facing discrimination

READ MORE: Why was my payday loan application denied?

Why Are Payday Loans So Much Easier to Qualify For than Traditional Loans?

Payday loan qualifications are minimal because the loans are very profitable for lenders. Lenders take advantage of borrowers’ desperation by charging them fees. The fees seem low to the borrower, who needs the cash and probably wouldn’t be eligible for a better loan. However, because the loans have to be repaid on your next payday, paying a $15 fee to borrow $100 for two weeks equals an interest rate of $391%. About 80% of payday loan borrowers can’t repay their original loans, and roll the loans over into new loans, with new fees.

Payday loans are estimated to be a $33 billion industry, according to Vantage Market Research, and that’s expected to grow to $42 billion by 2028.

How Do Payday Loans Differ from Other Types of Loans?

| Payday loans | Traditional loans |

| Small-dollar loans of $500 or less | Loan amounts up to $50,000 |

| Repaid in a lump sum in two weeks | Repaid in fixed installments over up to ten years |

| Require access to your bank account to automatically debit your loan payments | You aren’t required to provide access to your bank account |

| Charge fixed fees based on the amount you borrow; interest rates can exceed 600% APR | Charge interest rates ranging from 6% to 36% |

| No credit check | Usually require a minimum credit score of 580 |

| Costs are the same regardless of borrower’s creditworthiness | Borrowers with better credit scores will pay less to borrow money |

| Money is available within 30 minutes | Application approval can take several days |

| No collateral required | No collateral required |

| Don’t appear on credit reports | Appear on credit reports |

Why Are Payday Loans Bad?

Payday lenders prey on borrowers’ desperation. Target customers include:

- Americans who don’t have access to bank accounts

- Recent immigrants

- Undereducated individuals

- Families of Black or Hispanic descent

- Young adults struggling to repay student loans

- Low-income households

- Single parents

There are very few federal protections from payday lenders. However, some states have passed laws to help protect residents from predatory lending.

Payday loans are essentially banned in 21 states and the District of Columbia, either through specific laws or strict caps on payday loan interest rates.

Other states have passed laws regulating the industry.

For example, though payday loans are legal in California, the California Deferred Deposit Transaction Law strictly regulates the payday loan industry in the state.

Under the law, the amount of the consumer’s personal check cannot exceed $300 and a lender cannot charge a fee that is higher than 15% of the check amount. This means that if a borrower gives a lender a $300 check, the borrower will take home a cash loan of $255 if the lender charges the maximum fee. The loan term cannot be longer than 31 days.

On the other hand, Texas has few consumer protections, and payday loan interest rates in the Lone Star State can be as high as 600% APR.

READ MORE: States where payday loans are banned

Dangers of Payday Loans

Payday loans sound easy, but they come with a lot of risks. This includes:

- Racking up overdraft fees: When a lender automatically debits your account and the money isn’t there, it triggers a fee. Sometimes, they try to withdraw the money multiple times a day, racking up a fee each time

- Loan rollovers: When you get a new payday loan to repay a previous one, you’ll potentially pay the traditional fee, a late fee and a rollover fee. Suddenly, a borrower with a $300 loan and $45 fee can go from owing $345 to $500+ after paying off the original $300.

- Getting stuck in the payday loan debt trap: This is when payday loan borrowers constantly have to roll their loans over into new loans every payday. As the fees rack up, it gets more and more difficult to escape the cycle.

How Many Payday Loans Can I Get at Once?

You can technically have multiple payday loans at the same time, but it’s unlikely the same lender will give you two loans at once. You’d need to go to a second (or third) payday loan company to apply. However, this is not a strategy that we recommend. If you can’t pay your original payday loan, you have better options than getting a second loan.

READ MORE: If I have one payday loan, can I get another?

You Can Get a Payday Loan While Unemployed

Often, yes. Traditional financial institutions often reject loan applications from unemployed people, but payday loan lenders only require that you show that you have a regular source of income, depending on your state’s regulations.

Unemployed borrowers can, for instance, include Social Security as an income sources in their loan applications.

READ MORE: Can you get a payday loan while unemployed?

Why Do So Many People Use Payday Loans Despite the Dangers?

Most payday loan users have very few options or are unaware of other loan options that might be available. For example, credit unions offer a loan product called Payday Alternative Loans that are similar to payday loans but without the high fees. According to the National Credit Union Administration (NCUA) credit unions issued $227 million in PALs in 2022. But despite growing awareness, many Americans are still unfamiliar with Payday Alternative Loans and why they’re better than payday loans.

Is a Payday Loan Installment or Revolving?

Payday loans are neither installment loans nor revolving lines of credit.

Installment loans have fixed loan amounts and fixed repayment schedules. Examples include:

- Personal loans

- Student loans

- Car loans

- Mortgages

With revolving lines of credit, borrowers are given a credit limit such as $1,000 or $10,000, and they can borrow against that amount but don’t have to use all of it. A borrower only has to repay what they borrow, plus interest.

Payday loans don’t fall into either category. With payday loans, the full amount must be paid on the due date and the money can’t be reborrowed unless you apply for a totally new loan.

READ MORE: Is a payday loan installment or revolving

Do Payday Loans Affect Your Credit?

Payday loans won’t help your credit score, but they may hurt it if you don’t repay them as scheduled.

READ MORE: How payday loans affect your credit score

Most Popular Storefront Payday Lenders

Finding a reputable payday lender can be challenging. After all, there are more payday loan storefronts in the U.S. than McDonald’s or Starbucks.

Storefront payday lenders typically operate out of small stores and offer on-site applications and approval. Many of these lenders also use an online application.

Here are some of the most popular storefront lenders based on search volume.

Ace Cash Express

With 289,000 searches a month, Ace Cash Express is the most popular storefront lender on this list. The lender offers short-term payday loans to help underbanked consumers with small financial emergencies.

Pros

- Option to apply online or in person

- Lender offers short-term loans

- Borrower can decide to return the loan within 72 hours without penalty

Cons

- Website isn’t user-friendly

- Not available in all states

- Interest rates vary, but consumers with poor credit can expect to pay more especially for installment loans

- Lender doesn’t attempt to educate the consumer to help them with financial pitfalls or understand the risks of short-term loans

- In 2014, the Consumer Financial Protection Bureau took action against Ace Cash Express for using illegal debt collection methods, luring borrowers into payday debt traps, and encouraging employees to carry out these practices

Advance America

Headquartered in Spartanburg, S.C., Advance America is a popular storefront lender that specializes in payday loans, title loans, and installment loans. It has 202,000 searches per month.

Pros

- Operates in over 25 states with 2,000+ storefront locations across the U.S.

- Legitimate company established in 1977

- Superior customer service with quick response times

- Easy online and in-person application

- Many consumers receive funds the same day

- Provides useful resources online, including a repayment estimator which allows the borrower to calculate the interest on the life of their loan and make a payment plan before they borrow

Cons

- Automatic withdrawal from the borrower’s checking account when the loan is due

- Borrower must be a resident of the state they’re requesting funds in

- Interest rates are high and vary by state (in Alabama, for example, the APR is 456.25%)

- Some reviews mention the company is a scam, but these are from competitors and inaccurate

Speedy Cash

Founded in 1997, Speedy Cash is a privately held lender offering short-term payday and installment loans. The company has 160,000 searches per month.

Pros

- Multiple ways to apply, including in-person and on-site

- May obtain funds on the same business day

- No penalty for early payment

- Borrowers can receive funds via direct deposit, prepaid debit card, or in person

- Straightforward application

- Lender offers payday loans up to $500, depending on the state, as well as larger installment loans

Cons

- Certain states charge an origination fee, which is an upfront charge for processing a loan

- Not available in all states

- Sky-high interest rates

- Loan terms vary by state

- Not BBB-Accredited, though it has an A+ rating by customers on BBB.org

- Over 300 customer complaints in the past three years, mostly related to billing, loan collection, and predatory lending practices

- Was part of a class-action lawsuit in California for allegedly withdrawing hundreds of thousands of dollars from 1,000+ borrowers

Check Into Cash

Based in Tennessee, Check Into Cash was founded in 1993. It has 33,000 searches per month.

Pros

- BBB Accredited since 2000 with an overall positive customer review score

- Available in 20+ states

- Offers short-term online and in-store loans, specifically payday and title loans

- Loans vary from $50 to $1,000, depending on the state. First-time borrowers can borrow a maximum of $750 or their state’s upper limit

- Loan activity, including repayment and missed payments, is reported to a credit bureau

- Online educational resources for consumers

- Fast online and in-person approval

Cons

- Application requires a hard inquiry, which may impact the borrower’s credit score

- High payday loan fees (APR ranges from 153% to 1,042%, depending on the loan amount and state)

- Short-term payment options only

- Frequent miscommunications and loss of receipts

- May have additional fees for late payment or insufficient funds

- Inability to pay may result in the account going to collections

Check ’n Go

Operating under CNG Financial Corporation, Check ‘n Go is a non-BBB-accredited lender with 33,000 searches a month.

Pros

- Easy online or in-person application

- A bank account is not required if using a prepaid debit card

- Multiple short-term loans are available, including payday loans, installment loans, and cash advances

- Installment loans have a longer payoff term than payday loans

- Good credit isn’t necessary

- May receive funds within one or two business days

Cons

- Loan terms and tactics may be deceptive and lead to an ongoing debt trap

- Like other short-term lenders, Check ‘n Go is targeted at low-income, high-risk borrowers

- Extremely high interest rates

Most Popular Online Payday Loans

It can be difficult to find a good, trustworthy online payday lender. Particularly when tribal lenders are out there trying to trick you into loans with APRs of 700% or more.

Here are the top online payday lenders (that aren’t tribal lenders) based on search volume.

CashNetUSA

CashNetUSA offers payday loans to consumers with low or bad credit. It also offers flexible lines of credit and installment loans in some states. It has 100,000 searches a month.

Pros

- Same-day deposit is possible

- 31,000+ reviews on Trustpilot with an average rating of 4.5 stars

- Online application with instant approval

- 10-month to 28-month loan terms

- Maximum loan amount $500

Cons

- Loan terms and interest rates vary by state

- Not available in all states

- High origination fee on short-term loans (ex. $17.50 per $100 borrowed in Arkansas)

- 228% to 638% depending on the repayment period. Some claims of APR reaching over 1,100%

- One payment extension is available but with additional fees

OppLoans

OppLoans offers an alternative to payday loans up to $4,000. It has 95,000 searches per month.

Pros

- Fast approval and funding

- No credit check

- Reports to all three credit bureaus, which helps with credit building

- No prepayment or origination fees

- Offered in 36 states

- Great customer service

- Transparent loan terms and conditions

- Refinancing options are available

- Longer repayment options – up to 18 months – with the option of a hardship plan

Cons

- High interest rates in the triple digits

- Interest exceeds state maximums in certain states

- Required $1,500 monthly gross income

Net Credit

Based in Chicago, Net Credit has 51,000 searches per month. This lender offers short-term loans ranging from $1,000 to $10,000, depending on the state.

Pros

- Prequalification available

- Secure online application

- Consumers may apply for a line of credit up to $5,000, depending on the state

- Offers other loans up to $15,000

- Fast funding (within 1 business day)

- Long repayment periods (up to 5 years)

Cons

- High interest rates for a payday loan alternative (up to 36%)

- 10% cash advance fee

- $10 late fee

Rise Credit

Rise Credit has generally neutral to positive reviews regarding its online application process and customer service. It has 32,000 searches per month.

Pros

- Fast, easy application with approval in a few minutes

- Willing to work with no credit borrowers

- No prepayment fees

- 4000+ positive reviews on Trustpilot

Cons

- Loan terms are set and can’t be renegotiated

- High interest rates

- Terms and conditions vary by state

Possible Finance

Although Possible Finance offers payday-loan alternatives, its short-term financial solutions still come with a high level of interest and, as a result, risk. It has 29,000 searches per month.

Pros

- Ideal for borrowers with poor or no credit history

- Payday loans range from $50 to $500 on average

- Reports to all three credit bureaus

- May allow delayed payment

- Apply through their website or an app

- No early loan payoff fees

Cons

- APR is between 151% and 257%

- Only available in WA, TX, UT, ID, OH, FL, and CA

- Two-month repayment term. Website isn’t user-friendly or transparent with loan rates and fees

- Origination fee up to $20 per $100 borrowed

- Limited customer service

READ MORE: What are the best online payday loans

Are Online Payday Loans Safe?

From a technology and information security perspective, yes, they are generally safe, though there is an element of risk involved anytime you submit your personal bank account information and data via an online application.

One Speedy Cash customer was approved for a $300 payday loan, but the funds were never deposited into her bank account, and she found out that the lender was using incorrect information.

“They had my former last name and address, which I didn’t give them, and they said the first three numbers of my bank account number were incorrect,” the borrower said. “Now I cannot pay my rent, and my son and I face the possibility of being kicked out of our apartment.”

READ MORE: Are online payday loans safe

How to Spot Payday Loan Scams

To ensure the safety of your payday loans, it’s important to learn the warning signs of a payday loan scam. The Consumer Financial Protection Bureau (CFPB) offers a set of red flags.

These include:

- Requiring a payment or deposit before you get the money

- Asking you to pay “insurance” upfront to secure a lower interest rate

- Not telling you their name, employee ID number, or company information

- The name of their “company” is close to — but doesn’t exactly match the name of — a real financial institution

- The lender has an established online reputation with multiple verified reviews on sites like Trustpilot and the Better Business Bureau (BBB)

- Their website and online application are secured with HTTPS in the URL (not HTTP) and a lock icon in the address bar

- They have a physical address, even if they only lend online

- They’re a direct lender, rather than a third-party service

READ MORE: How to recognize — and avoid — payday loan scams

Better Payday Loan Alternatives (With No Credit Check)

- Bad credit loans

- Cash advance apps

- Buy Now Pay Later

- Earned Wage Access apps

- Credit card cash advance

- Peer-to-peer lending app

READ MORE: Payday loan alternatives

The Bottom Line

When you face unexpected expenses, a two-week loan to cover you until payday may seem like a lifeline. But the payday lending industry is designed to help you fail. The high interest rates and quick repayment deadlines make the loans almost impossible to repay.

READ MORE: How to get out of payday loan debt for good

FAQs

A statute of limitations is a law that restricts the amount of time that someone has to sue for damages they’ve suffered. This means that the statute of limitations on debt is the length of time a creditor or debt collector has to sue a borrower for defaulting on their account. It varies based on the state where you live.

READ MORE: What is the statute of limitations on debt?

Both are small loans, but microloans are designed to help low-income individuals start businesses, while payday loans are designed to give short-term credit between paychecks for immediate financial needs.

READ MORE: Microloans vs. payday loans

You can apply for a new payday loan as soon as you pay off the previous one. If you can’t pay off your current loan, your lender may let you roll it over into a new one.